Last week, I had the opportunity to give a talk on product innovation at the Fashion Institute of Design & Merchandising (FIDM). While I think they called me in to share some of the things I’ve learned during my time consulting to The Estee Lauder Companies, it’s hard to say who got more value out of the talk: the students or me.

I’ve switched industries a lot in my (admittedly) short career. Over the past few years, I’ve worked in higher education, early education, ad tech SaaS, cosmetics, and alcohol. Because of that frequent switching, I’ve often been a beginner and forced to get up to speed in new industries quickly. However, during the Q&A portion of the talk at FIDM, I realized I had stopped looking at the cosmetics industry through a beginner’s eyes. The students (all of whom were about 20 years old) were asking questions about the industry, sales channels, and technology from angles I had never thought of but seemed obvious as soon as they brought them up.

For example: among millennials, beauty influencers have huge power to drive sales, simply by recommending a product or featuring it in a makeup tutorial video. Several students brought up the (valid) point of diminishing consumer trust in influencers because of all the undisclosed sponsored posts. In hindsight, this concern seems obvious but in all my time working with beauty brands, this point has either been completely avoided or jokingly brushed off. Yet these students were able to very easily see the long-term consequences of the current influencer trend: diminished consumer trust. Instead of working with influencers or celebrities, these students were interested in figuring out how to build better peer-to-peer recommendation systems that start and end with product effectiveness in a personalized way and can’t be gamed by larger brands. Amazing concept!

What surprised me the most about the FIDM Q&A session is how unaware I was of losing my “beginner’s mind“. I’ve only been in the beauty industry for two and a half years – which is nothing if you compare it to colleagues who’ve been doing this for twenty or thirty years. But those two years were more than enough to make me miss obvious concerns with the current trendy marketing strategy. This brings up an important question: at what point do people lose their “beginner’s mind” and is it possible to keep this creative state of mind for longer periods of time?

At this point, I don’t quite know what the best solution is but I suspect it has something to do with continually exposing yourself to others without much experience and limiting your interactions with so-called “experts”. While I’m sure there’s some value in having deep knowledge within a specific field, it certainly does seem like the more time you spend working on a given problem, the more difficult it is to see the tangential opportunities that might be obvious to a beginner.

I’ll be exploring this beginner/expert dichotomy further in future posts but in the meantime, let me know your thoughts or experiences with the beginner’s mind on Twitter or in the comments!

For the typical early stage startup, closing a deal with a Fortune 500 company can provide a huge boost in morale and momentum (and hopefully cash). Enterprise deals are a signal for investors to indicate traction, a common source of free media attention, and a key factor when potential employees will weigh your offer against other opportunities.

Over the past several years, I’ve sat on the corporate side in my role building the External Innovation group at The Estee Lauder Companies, where I’ve worked on 200+ deals with startups of all sizes. Before that, I sat on the startup side of the table and led growth at several venture-backed companies; closing enterprise deals with companies like Proctor & Gamble, LinkedIn, Spotify, and Honda.

With this dual background, I’ve seen (and made) my fair share of mistakes in building startup-corporate interactions. Avoiding the mistakes below just might be the difference between celebrating a deal with a new enterprise customer and sitting on the sidelines wondering what happened. To paraphrase the classic sales quote from Glengarry Glen Ross: champagne is for closers.

Mistake #1: Assuming Large Companies Have Limitless Cash

Yes, you may be pitching to a billion-dollar company but the person you’re pitching to doesn’t have a billion-dollar budget. While corporate budgets may (keyword: may) have more wiggle room than startup budgets, your corporate counterparts are still dealing with many demands on a limited budget. On top of day-to-day budget concerns, large companies, even successful ones, may implement spending freezes for specific departments. It’s entirely possible that your potential customer will be comparing your product with something in a completely different industry, simply because you’re competing for the same budget dollars. Have some empathy for the budget concerns of your corporate counterparts and it’ll pay off by differentiating you from other salespeople they encounter.

Mistake #2: Trivializing Deep Corporate Knowledge

While it is possible that your startup is “changing the world”, the Fortune 500 companies you’re pitching to have already changed the world and know a thing or two about how things work. There’s nothing more annoying to your corporate counterpart than trivializing the deep knowledge they have of their industry. You can also run the risk of shooting yourself in the foot by extrapolating current trends in your presentation. Do you really think you’re the first person to tell a corporate innovation director with twenty years of experience that artificial intelligence is going to take over every industry by 2030? Whether you’re right or not, the point is they’ve heard that story before and may view it as a sign of arrogance. Showing some humility and using phrases like ‘our hypothesis’ go a long way towards establishing your honesty and credibility.

Mistake #3: Using Too Much Startup Jargon

True story: the first time I mentioned the word “accelerator” in a corporate R&D lab I was consulting for, a senior scientist gave me a confused look and said he “didn’t realize particle accelerators were funding startups now”. While this may initially make you facepalm, it was a great reminder that those of us in “startup world” truly live in a bubble that most of America, and the world, are not part of. Taking the startup jargon down a notch will help you get your point across.

It sounds cliché but knowing your audience is the key to effective communication. When pitching to individuals who’ve spent their entire careers in large companies, avoid using startup words that they won’t understand and connect with. It’s not the job of the audience to figure out the presenter – but it is the job of the salesperson to make sure their pitch isn’t going over the audience’s head.

Mistake #4: Ignoring Implementation Costs

In the omnichannel world we live in, any large company with a physical retail presence is constantly pitched new in-store technology concepts. While the startups offering these technologies are charging reasonable prices (often as low as $30/location/month), what is often ignored is the cost a company must incur to implement a new technology. For example, a technology that provides customer intelligence via iPad to in-store sales staff so they can sell better requires an extensive training program, troubleshooting, and potentially even in-store hardware upgrades. So even though a technology like this may only cost a total of $6,000 per month (200 locations x $30/location/month), the implementation costs (for things like hardware and training) across 200 locations could easily exceed $100,000.

Implementation costs are difficult to avoid entirely but there are steps startups can take to help their clients reduce costs and get themselves closer to signing a deal. These steps include negotiating reduced hardware pricing with manufacturers, assisting with or even providing free training, and offering to troubleshoot software issues for sales staff. Whatever you do, the important thing is to make it feasible and simple for the large company to say yes to working with you – and that doesn’t always involve the price of your actual product.

*****

Once you’re able to snag a meeting with a decision-maker at a large company, it means you’ve got their attention. They are interested (albeit at a very high level) in what your product can do. That said, these decision-makers are looking at dozens of other companies who are competing for the same budget. The easiest thing for a decision-maker to do is say no and any of the mistakes above give them an easy out. By always keeping your audience in mind, being empathetic to their concerns, and avoiding critical mistakes, your probability of closing a deal goes way up. And that’s ultimately the outcome that both large companies and startup salespeople are after.

The other day, I was looking to buy a jump rope I could travel with. After spending (wasting?) about 30 minutes going through jump ropes on Amazon caused by searching for “best MMA jump rope”, I paused to ask a highly relevant question: what in the world was wrong with me? Why did I need “the best” jump rope? The previous jump rope I owned came from who knows where and served me fine for a long, long time. The experience felt like living my own version of Aziz Ansari’s piece about trying to find the best toothbrush.

Last week, I had a great lunch conversation with my friend Lexi Lewtan (currently building AngelList’s A-List job platform) about something similar she was noticing in the recruiting industry. Companies all wanted to recruit “the best” iOS engineer or designer for their company even though that bar is subjective based on what that company is building. No one, not even early stage startups, wanted to settle for hiring an average engineer, even if that meant huge cost savings and would get the job done perfectly well.

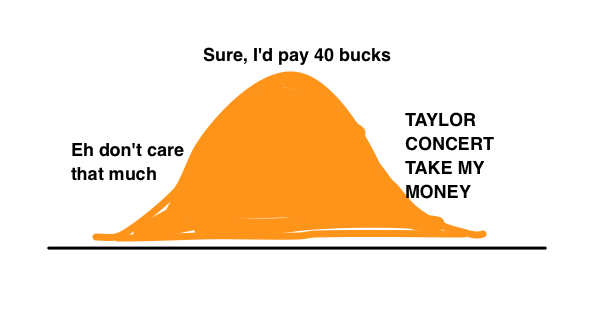

We’re taught in economics, entrepreneurship, and statistics classes to assume that most things lie on a normally distributed curve. This is especially true about demand – at some prices, I’d like to buy a “widget” while at higher prices, I wouldn’t.

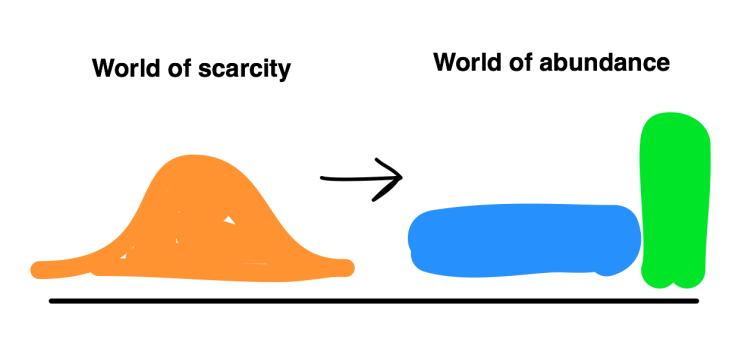

Essentially, the post boils down to the world moving from one of scarcity to one of abundance and that leading to a breakdown of the normal distribution curve:

Image Credit: Alex Danco

To build on Alex’s great post, I think we’re moving to an even greater dichotomy. We’re going to live in a world where companies AND people are either luxuries OR commodities. This trend is showing up in industries as varied as cosmetics, labor, food, and much more. Let’s start with some definitions; what’s the difference between a commodity or a luxury in this context?

Commodity: A product or service for which I’m brand agnostic and highly price sensitive, usually because I believe there is no major difference in quality between brands OR it’s just something I don’t really care about. Examples (for me): gas stations, drug stores, bottled water, socks, paper towels…the list goes on.

Luxury/Premium/Prestige: These are products or services for which I’m highly brand/review sensitive and minimally price sensitive. Things in this category for me include coffee, beer, shoes, cell phone, computer, chocolate, and many, many more. The luxury/premium/prestige category is the one where you would search for “the best” on Google or Amazon.

One key thing to remember is that the determination of a commodity or a luxury is an individual thing – for example, some people think all beer tastes the same and treat it as a commodity. I think differently and am willing to pay a huge premium for beer that I think tastes better, uses more valuable/rare ingredients, and has a better story behind its creation.

The easiest way to test whether something is a luxury or commodity for you is to imagine the price of product X increased by 10%. Would you still buy it or would you switch brands? For example, for most people, if a cup of Starbucks coffee increased from $2.50 to $2.75, they wouldn’t think twice about continuing to buy Starbucks. Similarly, if the price of a 15 inch Macbook Pro went up from $1,999 to $2,299, most Macbook Pro customers would still buy it (although probably with some complaining).

Let’s look at how the luxury vs commodity trend is affecting three very different industries:

Cosmetics

I’ve been spending much of my time studying the cosmetics industry because of my work at The Estee Lauder Companies. Since my role is to look externally, I’ve been watching how companies position themselves and how they’re adapting to this new luxury-commodity dichotomy.

One of the biggest moves last year in cosmetics was P&G divesting a huge chunk of their beauty business in a $12.5 billion sale to Coty. One of the striking things about that transaction is that P&G chose to hang on to its most prestige skincare brand – SKII. In another example, Unilever, a huge personal care company that traditionally stays in the mass-market world with brands like Axe, Dove, and Degree, bought 4 prestige beauty companies in 2015 and they’re on track to acquire more in the future.

For beauty brands, there isn’t much room left in the middle – either you’re making commodities that are competing on price (in which case, your gameplan should be to cut costs as much as humanly possible and sell at grocery stores and drug stores) or you’re competing on uniqueness and luxury, in which case you need some product, marketing, or service elements that stands out.

Labor

If you think about labor in a “prestige” vs “mass-market” manner, you see a similar thing happening. Companies look to hire world class full-time employees for a select few key positions and for everyone else, they’re OK working with outside firms or freelancers. This makes sense from their perspective: why invest additional overhead for average talent when you can replace it easily with the next person who walks in the door?

This trend is part of the reason we’ve seen marketplaces for unskilled labor pop up everywhere over the past few years – not just Uber, but also Fancy Hands, Handy, Wonder, and much more. The people working for these companies are all contractors, which is a much cheaper arrangement for companies than hiring full-time, allows flexibility for workers, and allows companies to adapt dynamically to demand in the marketplace (Uber’s surge pricing is the best known example of this).

On the other side of the unskilled labor marketplaces, highly skilled individuals in certain industries have seen their salaries climb higher and higher as firms bid for their talent. This can be seen on a wide scale by looking at software developer salaries or the long-term rise in CEO pay at Fortune 500 companies. As much as it would be fun to complain that these pay issues are all about corporate greed (which is certainly a factor for the CEO pay issue), at the end of the day, it’s really about companies bidding against each other for talent that they want to acquire or keep at all costs – aka the luxury talent.

Food & Beverage

Believe it or not, there was a time when coffee was a commodity item. For those of us who’ve grown up in the era of the $5+ latte, the commodity coffee era is a difficult world to imagine. I assure you, however, a world in which coffee consisted of hardly drinkable sludge that cost $0.50 was a very real place.

The late 80s and early 90s featured the rise of a company called Starbucks. You may have heard of them. The key distinctive trait of Starbucks was taking a commodity item that no one thought much about and elevating it to a level no other coffee retailer had imagined or done on such a large scale.

What does the word elevating mean? In this context, elevating coffee meant Starbucks started with higher quality beans than any of their existing competitors (luxury), roasted them with a more precise science than their competitors (luxury), integrated the story of Italy, espresso bars, and the Third Place (luxury), and included an ethical component (luxury). Compare that to a gas station that would pour some black sludge in a styrofoam cup and sell it to you for $0.50 (commodity). All of these elements factor into giving Starbucks the cache to sell a commodity product as an affordable luxury for almost 10x what their competitors were selling at. Howard Shultz (the man behind Starbucks) tells the full story behind the commodity to luxury rise in detail in his book Pour Your Heart Into It: How Starbucks Built a Company One Cup at a Time.

Today, the rest of the food & beverage industry is doing its best to try to break out of the world of commodity items. Whether they do or not remains to be seen but the tide has turned in luxury’s favor as more and more people are paying attention to the ingredients in their food. This creates an opportunity for brands to elevate (there’s that word again) healthy ingredients, the lack of preservatives, ethical sourcing, freshness, or dozens of other desirable food characteristics.

Commodity vs Luxury: The Way Forward

The main, short-term outcome of this commodity vs luxury transition is that companies are going to be forced to make decisions about how to invest in their futures. My guess is that more companies are going to invest in building brands that are luxuries. Why? Because a luxury’s key differentiator is uniqueness – which could come from a unique ingredient, a novel process, or a fascinating background story – any and all of which can be sustainable competitive advantages.

Building a commodity business seems to me as an outsider to be a lot more difficult. Commodity businesses would be competing mainly on price which makes it easy to imagine commodity businesses becoming a race to the bottom with margins getting slimmer and slimmer until there are no profits to be made. Commodity businesses survive on high volumes and while of course there will always be a (huge) market for them, I think we’re moving to a world where people will buy a higher percentage of products at a premium that last longer, work better, and are more unique – which by necessity means purchase volume will go down. This trend could also be tied to growing income inequality – fewer people in the middle class – but that requires more research to figure out.

Something I haven’t mentioned anywhere else in this post but runs in the background of all these trends is technology. Technology, especially data but also includes manufacturing tech like 3D printing, is giving companies the ability to create customized and personalized products in almost any industry – which is certainly one way to create a premium product. When a company has created a customized product for you and owns the data to continue improving that product, it becomes a premium experience with a competitive advantage. That’s a tough combination to beat.

Thanks to Lexi Lewtan, Brett Martin, and Josh Dodds for their feedback on early versions of this blog post.

Getting started in a new industry can be super challenging but in today’s world of shorter stints with companies, quickly building working knowledge of a new industry is an extremely valuable and essential skill. Becoming fluent in your industry quickly means you start providing value sooner to your team, customers, employers, investors – everyone.

Back in the day (2012), I showed up to a lunch meeting in Pittsburgh with Adam Paulisick unprepared to answer his questions about the economics of college admissions, the industry I was running a company in at the time. He gave me some advice that stuck with me ever since: To win, you HAVE to know more about your industry than anyone else – there are no excuses.

Since that embarrassing episode, I’ve tried to apply Adam’s advice to everything I’ve done and developed a step by step process that makes the challenging process of getting up to speed in a new industry a bit more methodical:

Step 1: Read as much as you can about the market

There’s nothing to replace this step. Read EVERYTHING – articles, journals, books, forums, industry history, even tweets. Don’t judge anything you read yet – at this point in the process, you don’t know anything. If there’s some kind of overview book, start with that – if not, start with articles because they’re usually written in layman’s terms. You should absolutely be taking notes – the key here is to start building a knowledge base. Allow yourself to go down the rabbit hole.

One last thing on this topic: give yourself the time you need to read about the industry. Study for this like you studied for the SAT and make sure you block the time off on your calendar. This is just as important as any meeting.

Step 2: Find people who know a lot about the market and spend time with them

Talking to knowledgeable people and asking questions is something that should be done mostly in parallel with reading but make sure you’ve at least read a little bit first so you can ask relevant questions. Don’t worry about forming opinions yet – just keep building knowledge. Asking someone for their time initially feels scary (why would they want to talk to me?) but you’ll find that smart people: a) generally want to be helpful and b) are generous with their time when they sense you’re genuinely curious about their life’s work.

A simple hack here that’s been magical for me: Ask each person you talk to in the industry for one other person they recommend you talk to. Even better, ask if they can introduce you. Very quickly, you’ll have a network of really smart people who genuinely want to help you learn. #winning

Step 3: Form opinions and test them

The first two steps in this process are fairly straightforward – they require work but your ego isn’t at stake. The third step is what will require some courage. To figure out if your mental “picture” of your new industry is correct, you’ll have to form some opinions AND get a reaction on those opinions from knowledgeable people. Without getting a reaction on your opinions, you’ll simply be forming a (likely) incomplete/incorrect mental map of the industry. Feedback is what allows you to correct, iterate, and improve on your mental map to create something resembling reality.

One of the most amazing things about the discovery process is that this is the stage where tons of ingenuity comes from, likely because at this stage, you’re reasoning from first principles (as opposed to ingrained dogma). Cherish this point of the process even though it’s scary sometimes. The worst-case scenario is that you say something stupid – no big deal.

Step 4: Repeat, repeat, repeat!

This process isn’t something that should only be done when you first start working in a new industry. It should be done constantly so that you continually grow your knowledge base and keep your mental map up to date. The ultimate goal is to have what athletes refer to as “fingertip feel” of your industry.

Bonus Tip: Your ego is your worst enemy

All of the suggestions above require leaving your ego at home. If you can’t do that, all the feedback in the world won’t improve your mental map of any industry. Remember, feedback isn’t an insult – it’s a gift and a huge competitive advantage. Allow yourself to accept feedback and you’ll find that you’ve learned more about your industry in 6 months than most people learn in 10 years.

On the surface of it, selling something is pretty weird. You’re basically using words, Jedi mind tricks, and (occasionally twisted) logic to convince someone that they should do something, which usually consists of them giving you money.

Oh and if you’re about to skip this post because you’re not a “salesperson”, let me ask you something: have you ever had a job interview? Have you ever pitched an idea? Have you ever asked your teacher for a deadline extension? Yea…you’re a salesperson. Don’t be ashamed, we’re all salespeople. Own it.

So if we absolutely have to do the uncomfortable act of selling something, we might as well do a good job right? The art of selling is first and foremost about confidence. If you don’t believe in what you’re selling, you can be damn sure no one else will either. Salespeople require a similar level of unshakeable confidence as athletes do and just like athletes, salespeople tend to have a “sales prep routine” to get into the right sales mindset. Here’s one that works for me:

Step 1: Watch these 2 videos (language NSFW) featuring Vin Diesel and Ben Affleck from the movie Boiler Room. Awesome demonstrations of sales techniques in here too:

Best quote from these videos: “There is no such thing as a no sales call. A sale is made on every call you make. Either you sell the client some stock or he sells you on a reason he can’t. Either way a sale is made”. Word.

Step 2: Review your plan – why should this person give you what you want?

I’m not a big believer in sales scripts. In my opinion, scripts are a great way to make yourself seem robotic and unlikeable (unless you know the script really, really well – so well that it’s second nature and you don’t have to think about it). That said, it’s still important to have a gameplan in place – where do you want the conversation to go, how you want it to flow, and what you want them to do. Most importantly, you have to be able to answer the question: why should the other person do what you want them to do?

Step 3: Review objections – why would someone say no to what you’re selling?

Inevitably when selling, someone is going to say no to you. The key is how you handle their objections. Obviously you need to know what the objection is in order to respond to it and improve in the future, so make sure you make the effort to find out. It amazes me how many people take “no” at face value in the sales process and completely miss the opportunity to iterate on their product/pitch. By understanding objections, at the very least you know what you can improve for next time. And yes, you should be writing these objections down.

Step 4: Watch Alec Baldwin motivate you to sell in Glengarry Glen Ross (language NSFW)

Remember: Always be closing!

On a more serious note though, the AIDA (Attention, Interest, Decision, Action) framework that Baldwin talks about is really, really effective. Learn it and use it.

Step 5: Go make the sale

You got this. Have fun with it – what’s the worst that’s gonna happen? They say no? Their loss.

Step 6: Drink some coffee (because coffee’s for closers only)

If you want to go deeper into learning sales skills, I highly, highly recommend buying Jeffrey Gitomer’s Sales Bible book and getting tons of real life practice. There aren’t any shortcuts to getting good at this stuff. It just takes confidence and hard work.

Over the past ~2 years, I’ve been working almost exclusively on customer development and growth at Mom Trusted, with my consulting clients, and at Workhorse. In 2015 alone, I’ve had upwards of 100 customer development conversations. Along the way, I’ve learned a few lessons, some from personal mistakes and a few from observing others.

Here are some of the pitfalls to avoid if you’re trying to learn something about your potential customers, instead of just paying lip service to the “customer development” buzzword.

Being Scared To Talk To Customers

This is, by far, the most unforgivable customer development sin. It’s impossible to get an accurate sense of reality without understanding, in extreme detail, the motivations and fears of your target customer. This fear of customer interaction lies in the fact that most founders (I’ve fallen into this trap in the past) have a mental picture of what their product/experience looks like and don’t want to burst that bubble. Maybe they also have a mental picture of what success will look like after they sell their company to Yahoo! for $100 million and don’t want to ruin that fantasy world by finding out that customers don’t want what they’re selling. Everyone has their own reasons for being scared to put themselves out there but this is the most dangerous sin on this list.

Putting A Layer Between You And The Customer

This is one I’ll never understand. I’ve come across founders, that for whatever reason, put a layer (or two) between them and potential customers. I don’t know if this stems from shyness or bubble bursting syndrome or what, but the net effect is that these founders always hear what their customers want or are frustrated with from some third party source. This is a great way to get incomplete or even plain wrong information, since the people who make up the layers (presumably employees or contractors) will try to tell you what you want to hear.

By not hearing any feedback directly, it’s easy to delude yourself into thinking things should be a certain way with no real evidence. In contrast, some of the best founders – including Jeff Bezos (Amazon), Steve Jobs, (Apple), and Tony Hsieh (Zappos) – correspond with their customers directly on a regular basis, even after their companies became multi-billion dollar Goliaths. Sorry, 10 person startup founders – there’s no excuse for not talking to customers directly.

Not Empathizing With The Customer

Empathy is such an underrated part of customer development. The problem with purely asking questions and using the responses to build your model of the target customer is that sometimes people don’t always verbalize the underlying emotional need they’re trying to express. For example, the success of Facebook can be very much attributed to people’s loneliness and desire to stay connected. But very few people would ever say that they use Facebook because they’re lonely. They would say they want to “stay in touch with family and friends” or “share important life events with people close to them”.

Customer development is all about building a complete model of the target customer. To build that complete model, you absolutely need to know the following:

What gets them out of bed in the morning?

What do they care about?

Who is their customer?

How are they measuring success?

What are they motivated by?

What keeps them up at night?

Empathy isn’t really something you can fake. Customers can tell if you’re just phoning it in and don’t really care about solving their problem. Be genuine and you’ll be pleasantly surprised by what they share with you.

Not Even Knowing Who Your Customer Is

This sounds dumb – how can you not know who your customer is? It’s actually a really common issue for B2B startups at the earliest stages. For example, imagine you have a software tool to help salespeople. If you’re taking a top-down approach where you sell to the VP of Sales and sign an enterprise contract, then your customer is not the junior salesperson, it’s the VP of Sales. If you’re taking the bottom-up approach and getting individual salespeople to use your tool and then drive adoption through their organization, your customer is the junior salesperson. You can see the end result of these alternative approaches by looking at the difference in UX between Salesforce and a tool like DocSend. To me (not a VP of Sales), DocSend looks awesome. Salesforce, on the other hand, does not. I’m not the target customer though – with the success Salesforce has had, it’s pretty obvious that their target customer likes them a lot.

By properly defining the customer, you can start to get accurate answers to your customer development questions, which is the first step to building a product that solves a problem for someone.

Closing Thoughts

Every company, whether it’s a startup or a Fortune 500 corporation, is 100% dependent on its customer. Having a thorough understanding of a customer, their life, and their motivations is the only way to create something they actually want. Remember: while potential customers usually have a fixed need they want fulfilled, which can be physical (for example, hunger) or emotional (loneliness), the form of the solution may change over time. The only way you’ll be able to understand the need and the form of the solution is by truly empathizing with your customers’ pain. It’s a skill that takes practice but it starts with something super simple: Ask questions and actually listen to what your customers tell you!

Most business books are unnecessary to read if you’re reading to learn something. When I say unnecessary, I don’t mean the information provided in them isn’t helpful. I mean that there’s nothing you can find in those books that couldn’t be learned from a couple of blog posts. I notice this more with newer books than older ones but that’s probably because the older books that have survived and are read today actually have some worthwhile ideas.

Most business books simply repeat ideas that have already been talked about 100 times elsewhere. Now that’s actually fine – IF the book expands on those ideas with longer anecdotes and examples OR it organizes the information in a way that makes it more accessible to the reader.

For example, Traction does a great job of organizing information in an accessible format. Everything contained in Traction can be found online from various sources. The real value of the book and having it available as a reference is that it pieces together information in a coherent format that saves you time and energy. Last time I checked on Amazon, Traction cost $10.64 for the hardcover edition. Would I pay $10.64 to have this set of resources on my desk any time I want? Hell yea – and it’s sitting on my desk right now.

Another example of a business book worth reading is Ben Horowitz’s The Hard Thing About Hard Things. Ben’s been in the trenches with a few companies and has some amazing stories to share – I can’t recommend this book enough if you’re a founder or have any thoughts of becoming a startup employee or founder someday. The book is about 300 pages long but when I finished, I found myself wishing it was longer because the examples and stories were so good.

Benedict Evans and Chris Dixon have some pretty entertaining tweets about business books and I think they’re spot on, Benedict’s quote in particular. Business books make “business people” (whatever that means) feel productive and good about their reading time. Kind of like most self-help books, they’re written in a way that makes sense and has you nodding your head until you actually think about the application and you realize that you just read a bunch of fluff.

Last week, I read Seth Godin’s Permission Marketing, which was written way back in 1999. It’s a smart book and was definitely revolutionary when it came out but probably 75% of it was unnecessary. The entire 200+ page book is about the concept of getting permission from consumers to market to them with the prime example being email newsletter signups. Solid concept but not nearly enough detailed examples to warrant 200 pages. I saw the same thing while reading The Lean Startup by Eric Ries. Another great concept but again, too much fluff.

While you shouldn’t categorically reject business books, be careful which ones you invest your time in. Often, you’re better off spending your time reading books about history, philosophy, psychology, or biographies if you’re reading to learn something. You’ll find that those are usually more relevant to solving your problems than business books are.

Ask anyone if they want to get something valuable without giving up a single penny in return and they will definitely say “yes”. It’s a human trait – we really love free stuff.

On the Internet, we’ve gotten used to getting products and tools for free. There’s nothing inherently wrong with this. Some companies are using a freemium model where they give away part of their product for free to entice you to buy the full product. Game companies do this all the time as do companies like Dropbox. Other companies give away their product for free in an effort to build an audience and sell ads – Google, Facebook, and Twitter for example. Although the ads can get annoying sometimes, these are all perfectly acceptable business models.

Where things get more dangerous and scary is when tools that involve sensitive information, such as healthcare, personal finance, or security are given out completely free. I want to be clear here: I’m not talking about freemium or free updates. I’m talking about 100%, no strings attached, free.

Why is this dangerous? Because companies need to make money and the easiest way for these “free” products to do it is by selling your personal data. In its most innocent form, this simply involves lead generation – think Mint.com and all the credit card offers you receive through their site after making an account. At a more insidious level, personally identifying or user activity data could be sold to third parties.

Don’t believe me? StopDataMining.Me was featured in Lifehacker last year identifying 50 data brokers who store and re-sell your personal data to others. They all have ways to opt-out but let’s be honest: how many of us even know the names of all the companies reselling our data? Even worse, you have to opt-out from each site, one by one. The problem is so widespread that The Federal Trade Commission issued a report earlier this year recommending that Congress require data brokers be more transparent and give consumers greater control over their personal information. Not much has happened with that so far but the recommendation by the FTC is a step in the right direction.

At the individual level, there’s not much we can do about all this except be aware of it. I’m not saying we should stop using free tools. Just be sure to think through the business model of whatever tool you’re deciding to use. My one recommendation would be to opt for paid tools and services for things that involve sensitive data – the extra few dollars per month is worth it.

True or False: Accomplishing your goal 30% of the time is good.

The answer: It depends. If you’re in school and only getting 30% of the answers correct, it’s probably time to stop reading this post and go hit the books. But if you’re a baseball player and have a batting average of 0.300, then you’re one of the better players.

Growth marketing, especially for startups, is more similar to baseball than it is to school. You’ll try tons of different tactics and strategies to grow – the phrase we use is “Throw s**t against the wall” – and most of it won’t improve your growth rate at all. Of the few things that do work, most of them won’t be scalable and allow you to grow 10X. Finding a scalable growth tactic that works is a bit like trying to find a needle in a haystack, except in this case, you don’t even know if there is a needle hidden in the haystack.

So if most things don’t work, how do you find the things that do? By doing lots of customer development and experimentation, which requires a completely different mentality than schoolwork. This was the most difficult leap for me – realizing that my answers were going to be wrong more often than they were right – and being OK with that. It’s hard to overstate the difficulty of this mental switch. We go to school for 12 years and then years of college and/or grad school with the “I should always get the right answer” mentality, which is counterproductive to being a good growth marketer.

The best way I found to handle this leap is to think like a scientist. I start with a theory, for example a new pricing strategy, and then develop an experiment and hypothesis to test that theory in the real world. Testing can only be done by putting your idea in front of customers/users. I try to pick a big enough sample size to make the experiment relevant (sample size depends on what you’re doing/selling) but keep it small enough to where I can speak with the customers individually to learn why they are saying yes or no. Unfortunately, thinking like a scientist is not taught in high school or undergrad, even if you major in science or engineering. It’s something you have to develop on your own.

The last piece of advice I’ll give on this is that successful growth requires thinking outside the box to find something that clicks (terrible pun…). At Mom Trusted, we experimented with phone, direct mail, email, fax, social marketing, SEM, SEO, conferences, and many many more tactics (with lots of iterations in each of those categories) in order to find the channels that worked. Other companies, like Eat24, have gone even more outside the box by advertising on overlooked web properties (including porn sites). All of these tactics were figured out through data-informed (not data driven) experimentation.

Thinking about growth marketing like a scientist is a skill and like any skill, it can be developed through practice and study, with practice being more useful than study. If growth is something you’re interested in, I strongly recommend getting real world experience as soon as possible.

Lately, there’s been some much needed talk in the startup community about the mental health effects of the constant ups and downs that come with being involved in early stage companies. The toll can be especially taxing on founders – take a look at the notes Brad Feld received from founders after he wrote his illuminating “Founder Suicides” blog post earlier this month.

The media usually portrays famous founders as Supermen/Superwomen – which makes “regular” founders feel inferior and inadequate. This is very much related to the “crushing it” culture that has gotten so rampant. When founders are asked how things are going, it’s incredibly rare to hear an answer other than one of the many variations of “crushing it”. With more people like Brad Feld talking about mental health, I’m hoping that honesty will become more common, but maybe that’s wishful thinking.

Having been involved in a couple startups over the past few years, I’ve been through some awesome experiences and also through shitty, terrible things that I wouldn’t wish on my worst enemy. Staying mentally healthy in a rollercoaster environment like that is a huge challenge and to be honest, is something I’ve struggled with at various times in my life. Over the past few months, I’ve taken a more active approach to keeping a healthy mindset. Below are some scientifically untested techniques I’ve been using with success so far to keep my work problems in perspective:

Read Books:

I read a lot of books growing up but for some reason I pretty much stopped once I got to college. In 2014, I rediscovered my love for reading and it’s been great. Most importantly, I’ve found it’s a perfect escape for my overactive work brain. When I watch TV or a movie, my brain doesn’t have to do any work and continues drifting towards work. When I’m reading a book, my imagination gets involved and my brain stops thinking about work for awhile.

Stay Physically Healthy/Exercise/Go Outside:

When you’re already not in a great mental state and then something goes wrong physically, you’re just asking for disaster. Re-committing to my health after some issues in early 2014 has helped my mental game so much.

Going out into nature is really helpful to me as well. There’s something about being in nature that just gives perspective and makes problems feel insignificant.

Get a Hobby:

Doing something outside of work gives you two things:

Your brain gets a break from thinking about the same problems – which actually helps you solve them.

You make friends outside the startup bubble

I started taking acting lessons in April and it’s been great. I’ve met people who live in a completely different universe from the startup community, which is enlightening. It’s also given me insight on my own emotions and habits that I wasn’t previously aware of. I started this hobby so randomly: I took a four week Acting for Non-Actors class to improve my sales skills and ended up liking it so much that I started training more seriously. Most importantly, it lets me shut off the analytical part of my brain for awhile and do something different.

Stay Close With Your Family and Friends:

This is listed last but it’s by far the most important one for me. In most industries (including startup world), things work like this: when things are going well, you have a ton of people contacting you and it feels like you’re the most popular person ever. But when things are going badly, no one wants to talk and you feel like an outcast.

The good news is that relationships with your true friends and family don’t change when things are going great or when things are going terribly. They will be there for you. This is why it’s so important to not let your relationships die out of laziness or lack of time – something that happens too often. Friends and family are your mental safety net. When I’m having a crappy day, nothing cheers me up more than gchatting/texting/Snapchatting with friends or having a long phone conversation with my mom, dad, and brother. Invest time in your relationships and you’ll never feel alone.

Lastly, I just want to say that having struggled with some of these issues myself in the past, I’m always here if someone needs to talk or get things off their chest.